Source: U.S. Energy Information

Administration and North American Electric Reliability Corporation, 2012 Long-Term Reliability Assessment

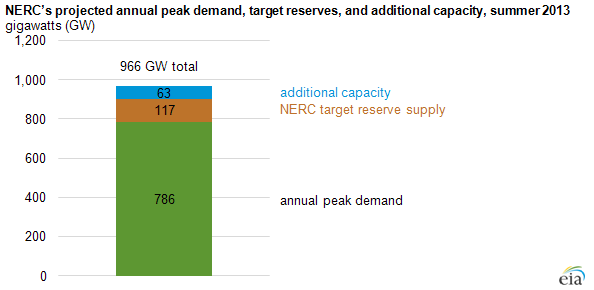

The North American Electric Reliability Corporation (NERC), the electric reliability organization certified by the Federal Energy Regulatory Commission to establish and enforce reliability standards for three major electrical interconnections serving the United States, issues a reliability assessment each year. NERC estimated in November 2012 that the United States would have 966 gigawatts (GW) of electric supply capacity available for the summer of 2013. NERC estimated that about 786 GW would be needed to meet projected peak electricity demand and determined that another 117 GW should be available in case of supply outages or extreme weather (known as target reserve supply).

The United States has 63 GW of capacity above and beyond the NERC target reserve supply. The electricity industry has reserve capacity on hand to maintain reliability. Because large-scale electricity storage is not currently economic, electric systems must have sufficient supply resources available to meet electricity demand and replace unexpected losses of supply. Each NERC region has a reserve margin target—the amount of supply capacity over and above a region's expected hourly peak demand for the year needed for reliability. The NERC regions' reserve margin targets typically range from 14%-17% and together total 117 GW of supply capacity.

There are several reasons why the total electric supply capacity within a particular region may exceed NERC's target capacity level. These include:

- Changes in demand growth. Demand within a region may grow more slowly than had been anticipated when capacity was added, or demand may even decline with changes in regional demographics and economic activity.

- Time lags in investment. New generating units with low operating costs are lumpy investments: they have high capital costs, regulatory procedures, and long lead times, making it challenging to match the timing and level of supply additions to meet expected increases in demand. This is especially true for units providing large increments of capacity, such as nuclear and coal generators.

- Past trends in capacity builds. Some of the current above-target supply is also the result of a building spurt for natural gas capacity between 1999 and 2003, driven partly by the desire of new competitive suppliers to gain market share. In recent years, supply additions in wind and solar capacity were spurred by both state-level Renewable Portfolio Standards and federal tax incentives. (DOE-EIA)

No comments:

Post a Comment